MIT 14.01 Principles of Microeconomics | Fall 2023 | Prof. Jonathan Gruber

Lecture 8: Competition II

한국어Core Message

"In the long run, if you're ever making money, more firms are going to enter until profits are driven to zero."

This lecture extends perfect competition to the long run by adding the assumption of free entry and exit. We show how this drives long-run profits to zero, and then examine three real-world complications that allow firms to earn profits even in the long run.

1. From Short Run to Long Run

1.1 Review: Perfect Competition Assumptions

Short-run assumptions (from Lec 7):

- Identical products

- Full information about prices

- No transaction costs

1.2 The New Long-Run Assumption

Free Entry and Exit

In the long run, firms are free to enter or leave the market

1.3 The Immediate Implication

- When do firms enter? When π > 0 (profits are positive)

- When do firms exit? When π < 0 (losses)

- What does this mean? In the long run, π = 0

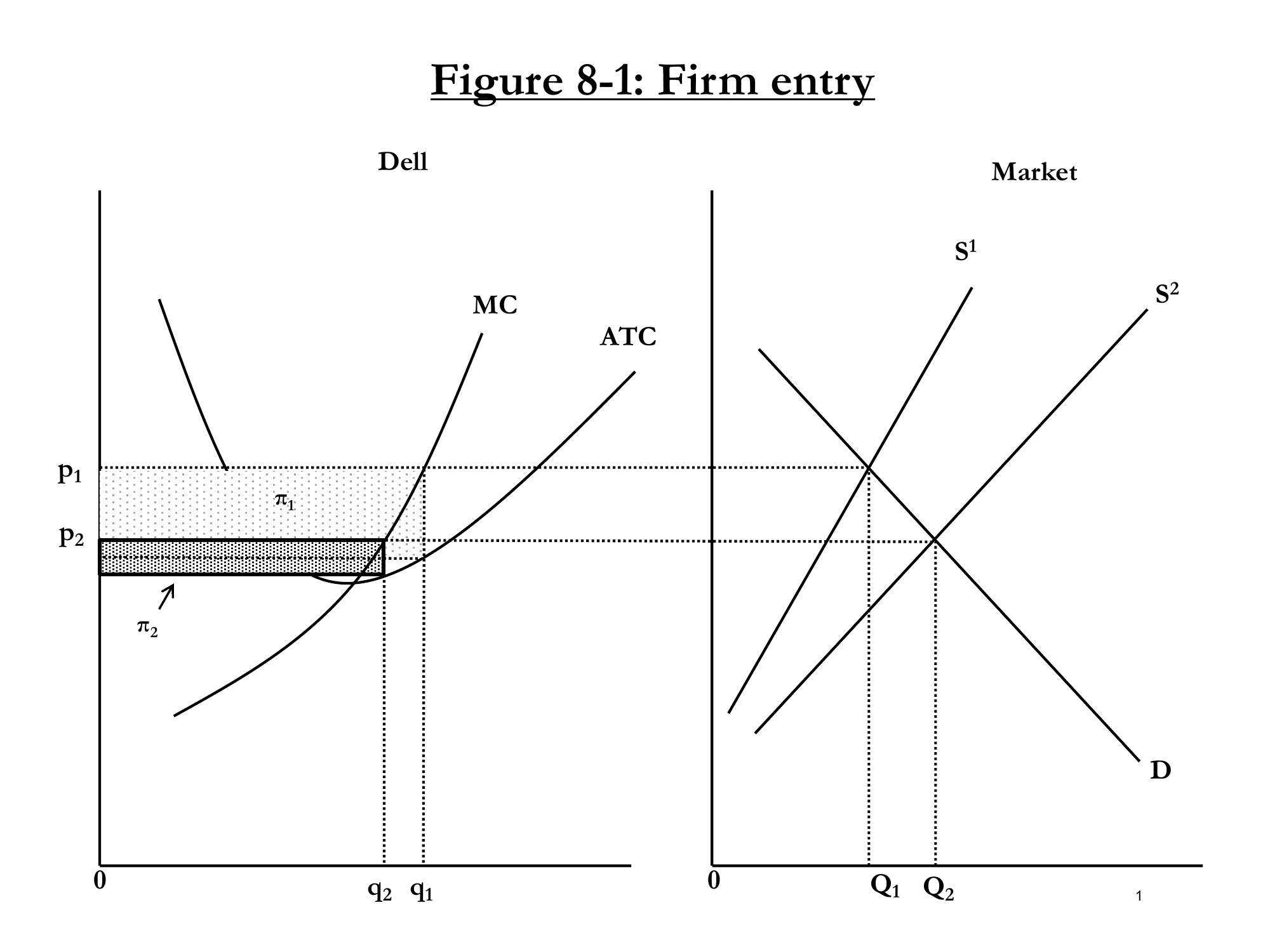

2. Firm Entry: The PC Market Example

"The market for personal computers circa 1990. This is just when personal computers were starting to take off. There were only a few firms — Dell, Gateway..."

Figure 8-1: Left: Dell's profit shrinks as more firms enter. Right: Market supply curve flattens.

2.1 The Entry Mechanism (Step by Step)

Step 1: Initial Equilibrium

- Dell produces at q₁ where P₁ = MC

- Profits = π₁ (the large shaded rectangle)

- Market: Supply S¹ intersects demand at Q₁

Step 2: Entry Occurs

- Positive profits attract new firms

- More firms → supply curve flattens to S²

Step 3: New Equilibrium

- Price falls to P₂

- Dell now produces less: q₂ < q₁

- Dell's profits shrink: π₂ < π₁

- But market quantity rises: Q₂ > Q₁ (more firms!)

Key Insight:

Little q↓ but Big Q↑ — each firm produces less, but total market output rises because there are more firms.

2.2 When Does Entry Stop?

"There's still profits. So what's going to happen? More firms are going to enter. And firms are going to enter until profits are zero."

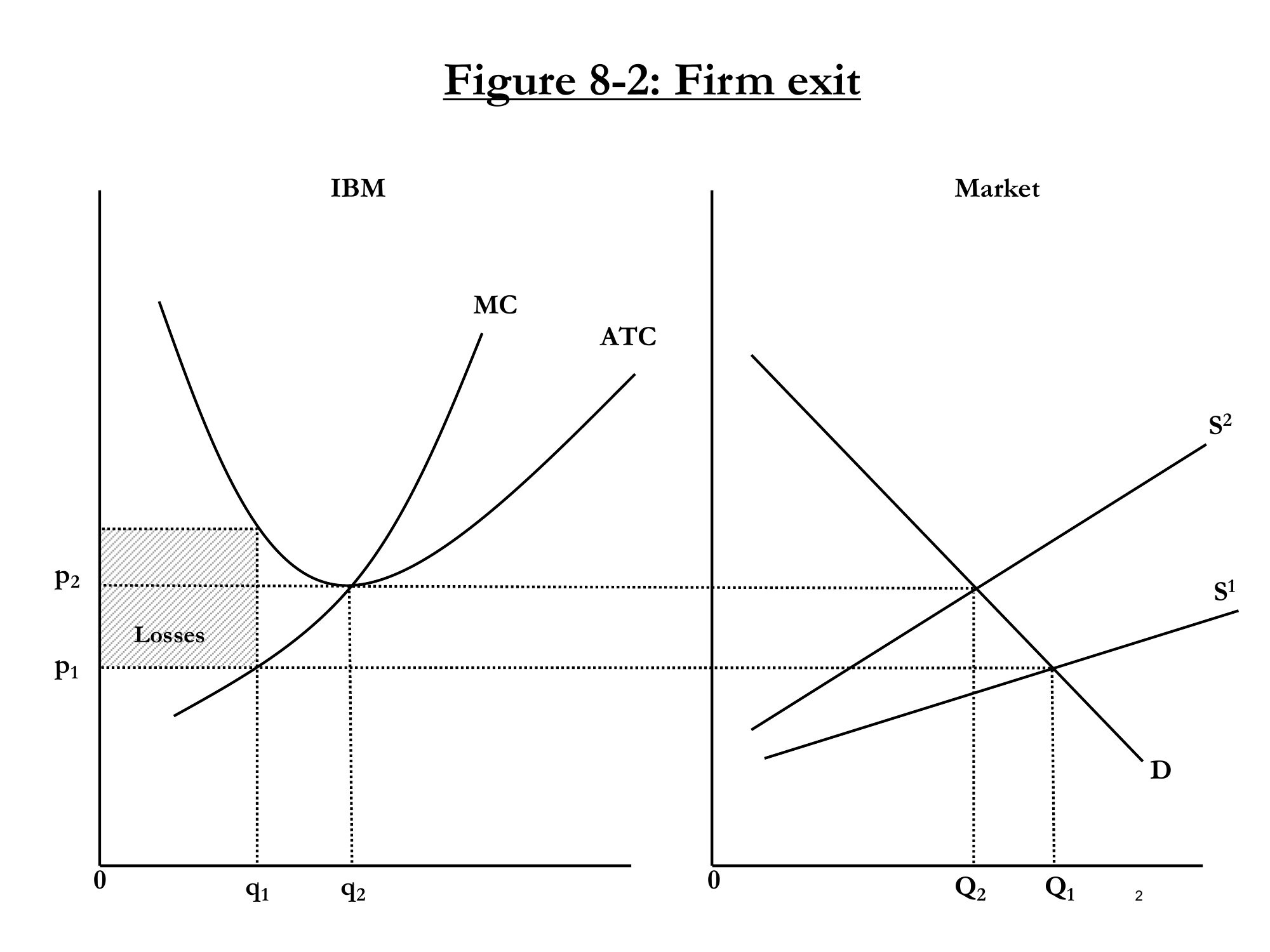

3. Firm Exit: The Mainframe Computer Example

"Ken Olsen founded DEC... The first lesson of graduation speeches, if any of you should ever give them — you don't spend the whole speech just talking about how wonderful you are. Well, that's what he did. He spent that speech on how wonderful he was, how DEC was incredible, how awesome they were. Five years later, they were basically out of business. Why? Because they got wiped out by PCs."

Figure 8-2: IBM losing money in mainframes. Firms exit → supply steepens → price rises → losses disappear.

3.1 The Exit Mechanism

Initial situation:

- Price P₁ is below ATC at IBM's production level

- IBM is losing money (shaded "Losses" area)

- Note: They're still above AVC, so they don't shut down in SR

Exit process:

- Firms like DEC exit the market

- Fewer firms → supply curve steepens (S¹ → S²)

- Price rises to P₂

- At P₂: P = MC = ATC → profits = 0

4. Long-Run Equilibrium: Zero Profits

4.1 The Logic Chain

π = 0 → P = AC → MC = AC → Min AC

- Entry/exit drives profits to zero

- Zero profits means P = AC

- Firms produce where P = MC

- So MC = AC, which only happens at minimum AC

In long-run equilibrium, every firm produces at minimum average cost (maximum efficiency)

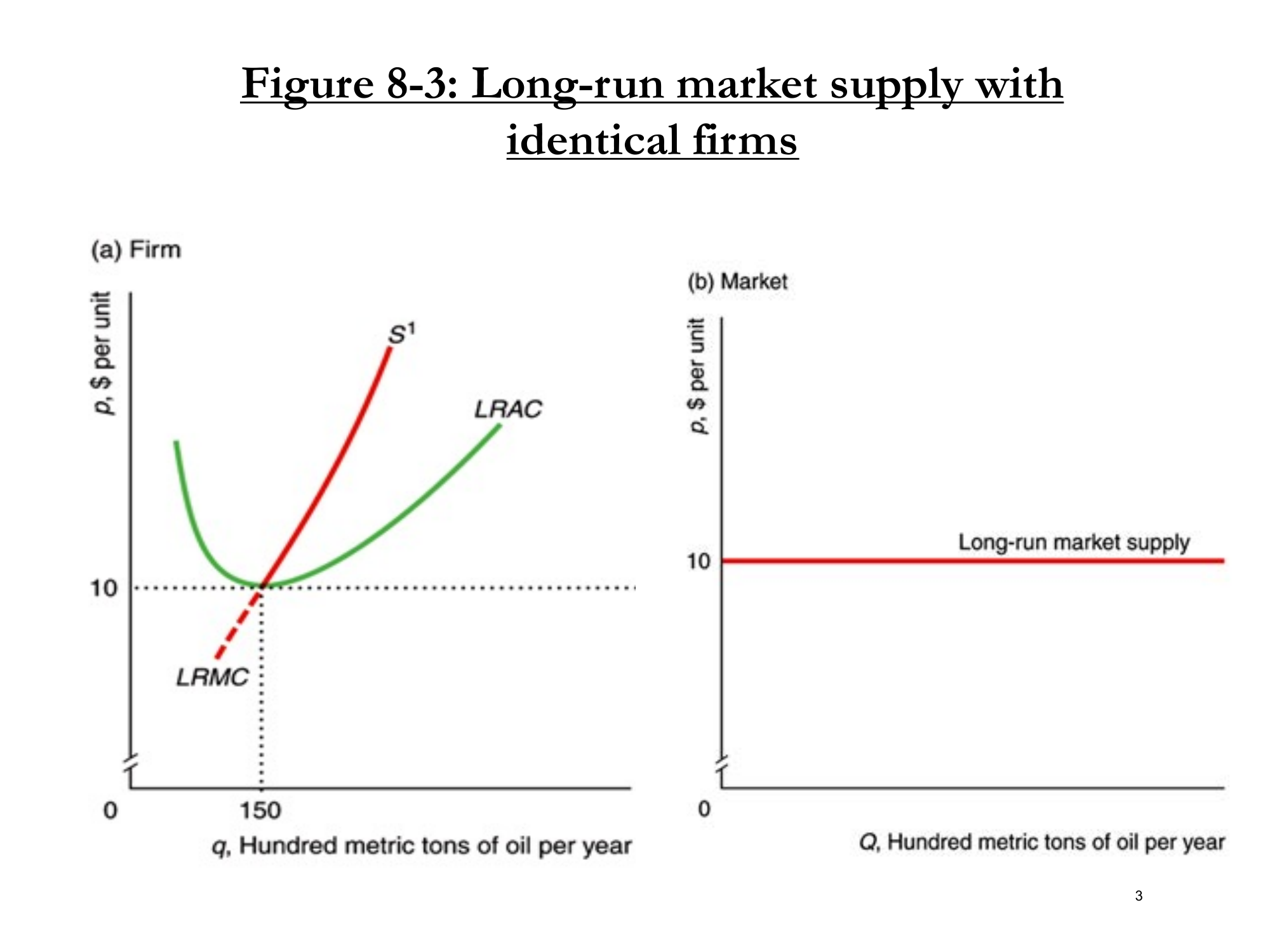

4.2 The Flat Long-Run Supply Curve

Figure 8-3: With identical firms, the long-run market supply curve is perfectly elastic (flat) at minimum LRAC.

- Firm level: Each firm produces at min LRAC (e.g., 150 units at $10)

- Market level: Horizontal line at min LRAC

- Why flat? Any price above $10 → entry → price falls back to $10

5. Reality Check: Why Aren't Profits Zero?

"Apple makes ungodly amounts of money. Tons of companies make ungodly amounts of money. So I bought your pizza cookies thing. But this is getting ridiculous. I can't buy a model where companies don't make profits."

Three Reasons for Long-Run Positive Profits

| # | Reason | LR Profits? | LR Supply? |

|---|---|---|---|

| 1 | Barriers to Entry | π > 0 | Upward sloping |

| 2 | Firms Not Identical | π > 0 (for efficient firms) | Upward sloping (step) |

| 3 | Input Prices Rise with Q | π = 0 | Upward sloping |

6. Reason 1: Barriers to Entry

Barriers to entry are costs that prevent new firms from entering a market.

6.1 The Ultimate Barrier: Sunk Costs

"Think about becoming a doctor. If profits of being a doctor aren't very big, you're not going to sink $300 grand into med school. So as long as profits aren't too big, you won't go become a doctor. So profits can't be enormous. But they can be driven not all the way to zero."

6.2 Examples of Barriers

| Industry | Barrier |

|---|---|

| Medicine | Med school costs ($300K+), licensing |

| Pharmaceuticals | Patents (legal monopoly) |

| Eiffel Tower souvenirs | Physical intimidation! |

| Tech (Apple, Google) | Network effects, brand, R&D costs |

Result: Entry stops before π = 0. Profits remain positive in long run.

7. Reason 2: Firms Are Not Identical

If firms have different minimum average costs, then efficient firms can make profits even when the marginal firm earns zero.

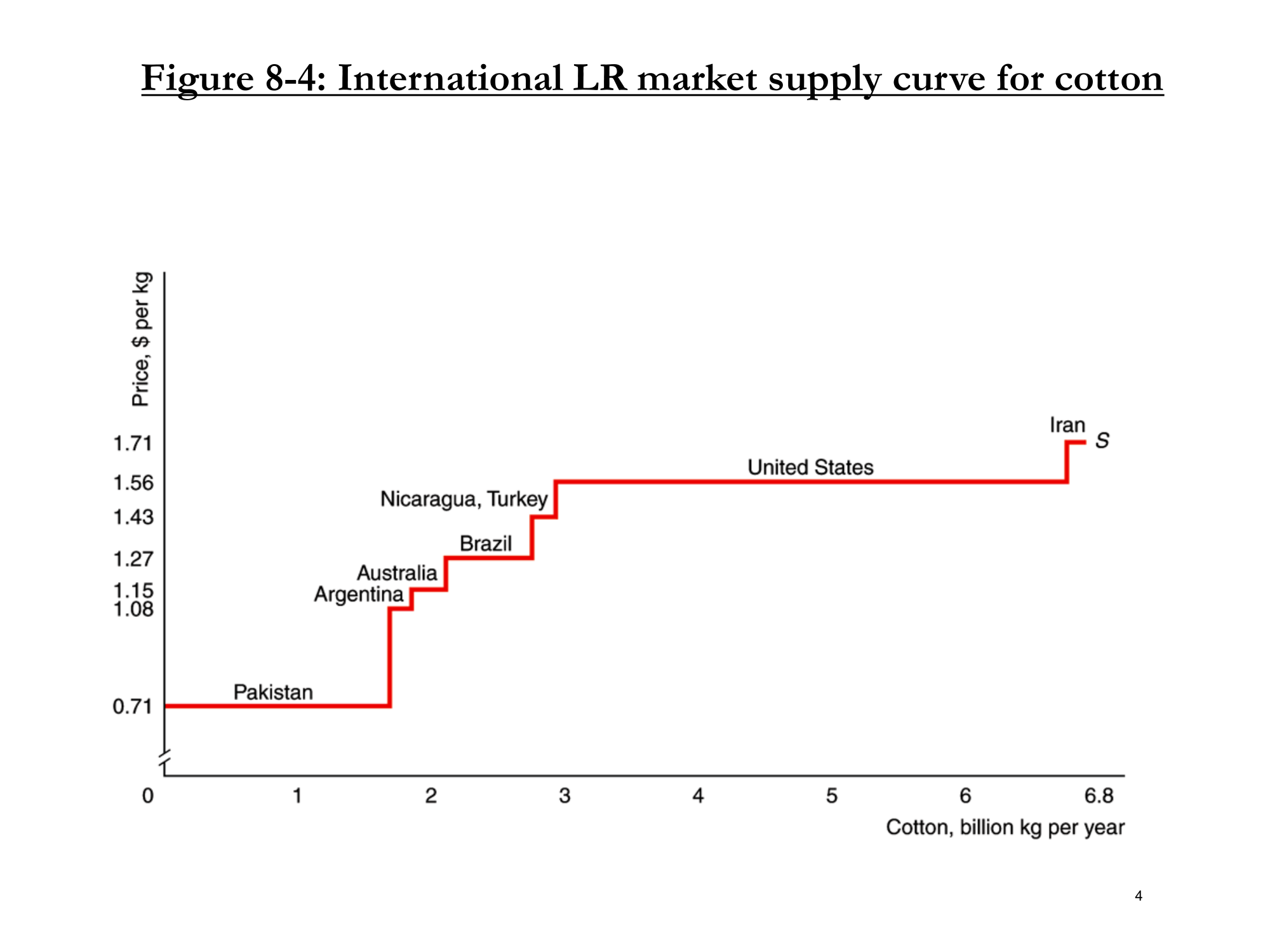

7.1 The International Cotton Example

Figure 8-4: Step-function supply curve. Countries have different production costs.

7.2 Two Scenarios

Scenario A: Demand = 1 billion kg/year

- Only Pakistan produces (cheapest at $0.71/kg)

- Price = $0.71

- Pakistan's profit = 0 (P = MC = AC)

Scenario B: Demand = 5 billion kg/year

- Need all countries up to US to produce

- Price = $1.56 (US's marginal cost)

- US profit = 0

- Pakistan's profit = $1.56 - $0.71 = $0.85/kg

Result: Efficient producers (Pakistan) earn positive profits when demand is high enough to require less efficient producers.

8. Reason 3: Input Prices Rise with Quantity

This is different from reasons 1 & 2: profits are still zero, but the supply curve is upward sloping!

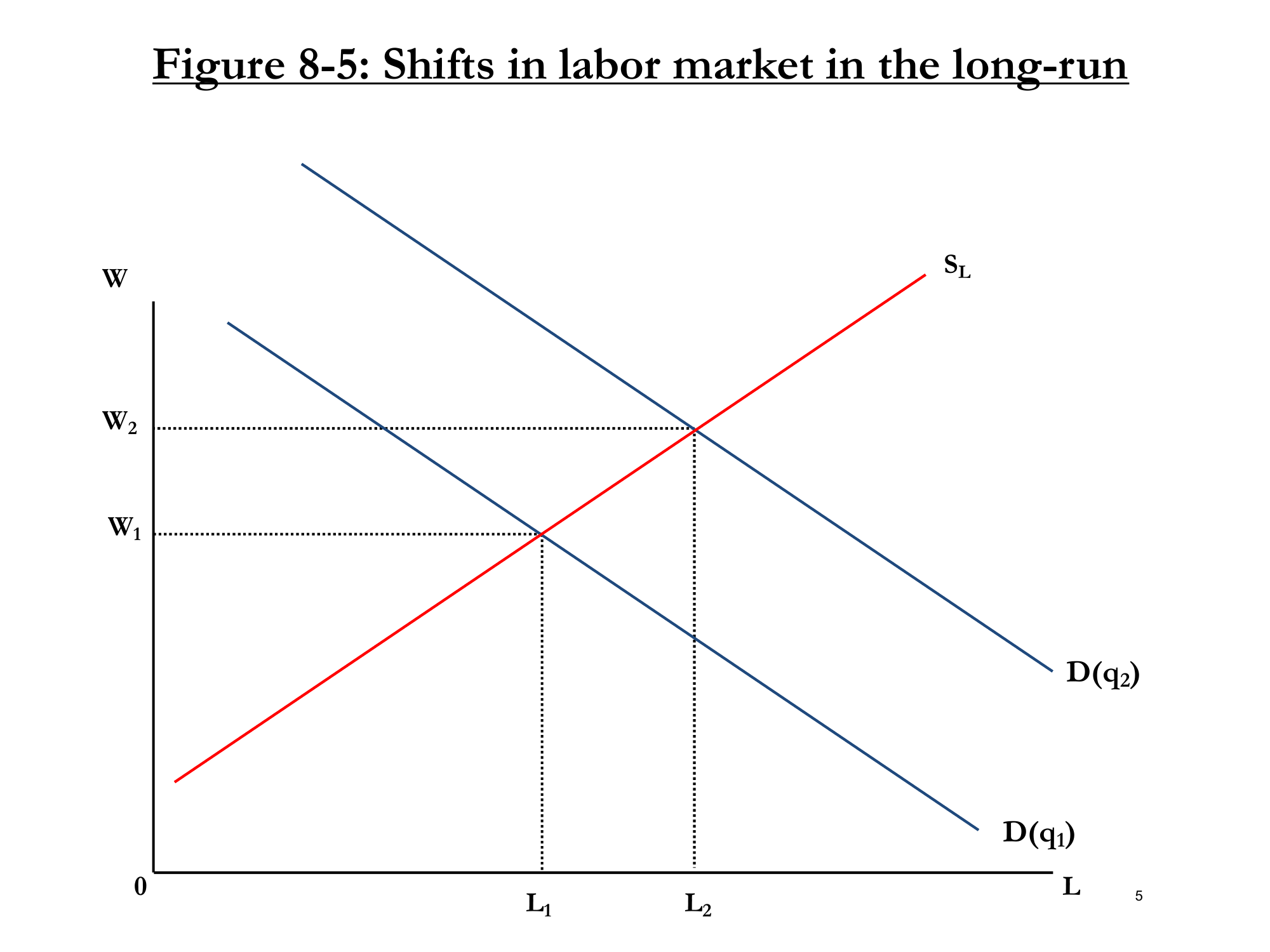

8.1 The Labor Market Link

Figure 8-5: To hire more workers (L₁ → L₂), firms must pay higher wages (W₁ → W₂).

The mechanism:

- Demand for goods increases

- Firms need more workers

- Labor demand shifts out (D(q₁) → D(q₂))

- With upward-sloping labor supply, wages rise (W₁ → W₂)

- Higher wages → higher MC and AC for firms

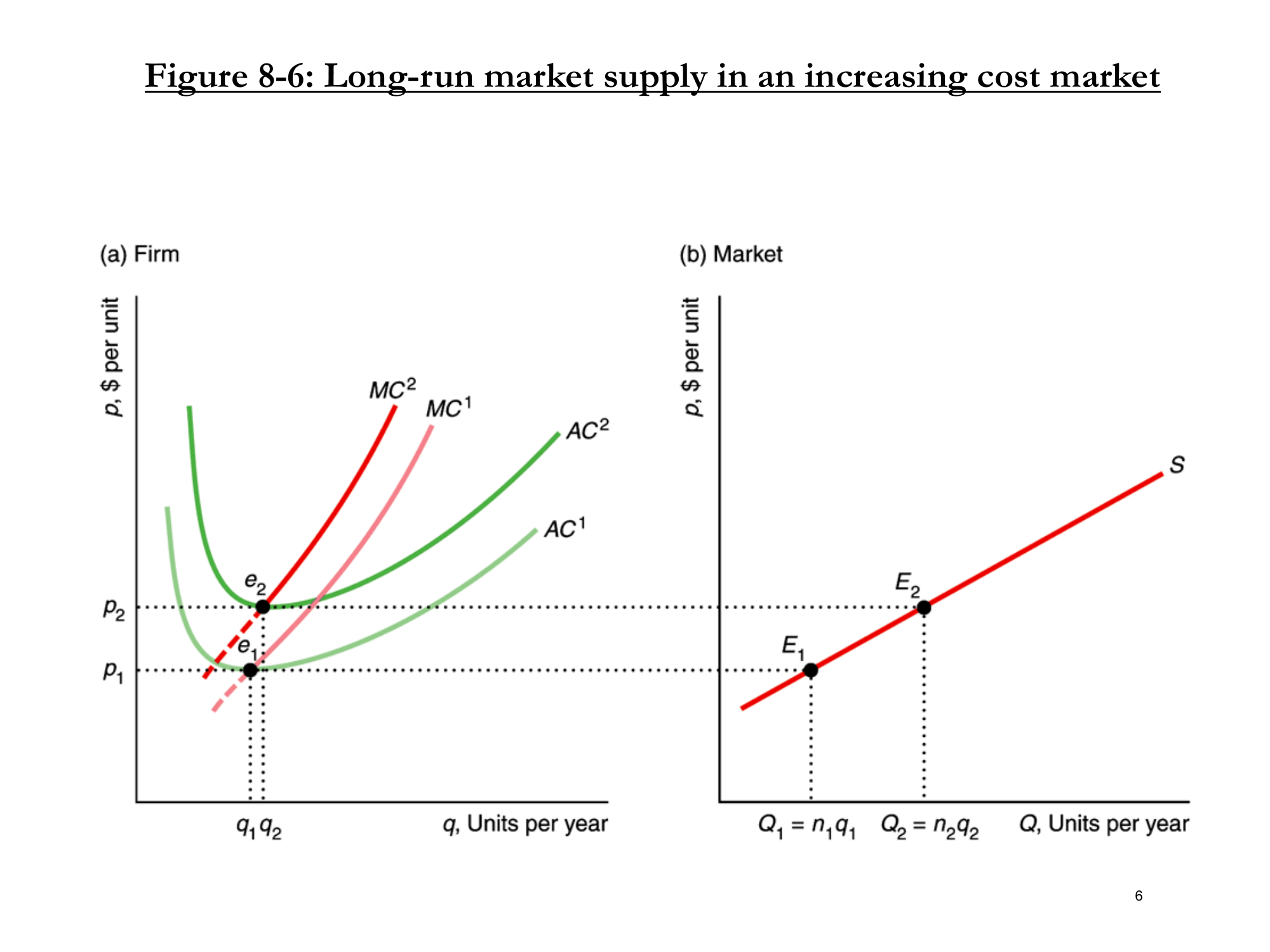

8.2 The Resulting Supply Curve

Figure 8-6: As output rises, cost curves shift up. Supply is upward sloping, but profits remain zero.

At equilibrium e₁: P₁ = MC¹ = min AC¹ → π = 0

At equilibrium e₂: P₂ = MC² = min AC² → π = 0

But P₂ > P₁ because costs have risen!

Critical Distinction:

- Reasons 1 & 2: Upward-sloping supply AND positive profits

- Reason 3: Upward-sloping supply but ZERO profits

Don't assume upward-sloping LR supply means positive profits!

9. Do Firms Actually Maximize Profits?

9.1 Suspicious CEO Compensation

- Amgen (2010): Lost 3% market value, 7% over 5 years → CEO made $21 million

- Abercrombie & Fitch (2008): Stock dropped 71% → CEO paid $72 million ("That's a lot of money based off good abs, right?")

- Leo Apotheker: CEO of HP for 11 months, fired for disaster → $13 million

9.2 But Maybe They're Worth It?

The Michael Jordan Example:

- Highest paid NBA player at one point: $32 million/year

- Academic study measured ad revenues from increased viewership when Jordan was on TV

- Result: He was worth $100 million/year

- So he was actually underpaid at $32 million!

"Just because someone's paid a lot doesn't mean they're not worth it."

9.3 The Agency Problem

"Corporations are owned by a disembodied set of stockholders. But the decisions are made by employees, managers who work at those firms. And that separation of ownership and control leads to a fundamental challenge."

Separation of Ownership and Control

Owners (shareholders) ≠ Decision-makers (managers)

9.4 The Private Jet Example

"Imagine you're a corporate manager at a pretty big but not massive company. It's big enough that you don't yet have a private jet. But all your buddies at the bigger companies have private jets. And they rag on you mercilessly, like, 'you loser, you don't have a private jet, you're nobody...'

"The problem is you've done the math, and it's not economical to have a private jet. You can fly first class anywhere for less. But you've noticed that if you change things a little bit so you flew only at the busiest times and only the most expensive airlines... the cost of flying commercial would be more than the cost of a private jet.

"So you make a PowerPoint. The owners could take the time to reverse engineer your calculations and figure out that you cooked them a little bit. But they're not going to. They're a bunch of disembodied people owning tons of stocks. So yeah, you make sense. Get a private jet."

Key Insight: What makes the manager best off ≠ what maximizes profit

9.5 The Richard Grasso Story

- Grasso: Great American success story — from shipping department to running NYSE

- Retirement package: $187 million

- Board of directors said: "We had no idea. We were just told it was this retirement package with a bunch of options and stock pieces. We couldn't unpack it."

"It's in the manager's incentive — it's his whole life's work to maximize his happiness. The board of directors, it's something they're doing part-time while they go play golf the other times."

9.6 Evidence: The Oil Price Test

Bertrand & Mullainathan's clever test:

- When oil prices go up, oil company profits rise

- But CEOs didn't cause the price increase!

- Yet CEOs get massive raises when oil prices rise

- This can't be paying for performance → must be agency problem

9.7 Attempted Solutions

| Solution | Idea | Problem |

|---|---|---|

| Board of Directors | Monitor managers on behalf of owners | Board members chosen by managers, often "corporate buddies" |

| Stock Options | Align manager incentives with stock price | Managers can manipulate short-term price (Enron scandal) |

9.8 The Enron Disaster

How stock options backfired:

- Enron managers had stock options → incentive to raise stock price

- Set up Ponzi scheme: Enron sold goods to its own subsidiaries

- Looked like big sales, but Enron was also booking the purchases

- Stock price went through the roof → managers got super rich

- Eventually exposed → company went bankrupt

"The problem with stock options is they work in theory. In principle, they can lead to even more bad behavior."

Academic Note: Bengt Holmström (Gruber's former colleague at MIT) won the Nobel Prize for understanding this fundamental tension. This is a huge area in corporate finance!

9.9 Accounting vs Economic Profits

Student question: How do you tell economic opportunity cost from accounting profits?

"Apple's $18 billion per quarter profits are accounting profits. What are economic profits? That's much harder to measure.

"But accounting profits aren't easy either. Apple reports $18 billion to their stockholders. To the US government? They report profits of essentially 0. Why? They pretend they have a company in Ireland with two employees. Ireland has low taxes. They claim all their profits are earned in Ireland from 'intellectual property.'"

Key Takeaways

| # | Concept | Key Point |

|---|---|---|

| 1 | Free Entry/Exit | New assumption for LR perfect competition |

| 2 | LR Zero Profits | Entry continues until π = 0; exit until π = 0 |

| 3 | LR Equilibrium | P = MC = min AC; all firms at max efficiency |

| 4 | Barriers to Entry | Allow positive LR profits (sunk costs, patents) |

| 5 | Non-Identical Firms | Efficient firms profit when demand requires inefficient ones |

| 6 | Increasing Cost Industry | Input prices rise → upward LR supply, BUT π = 0 |

| 7 | Agency Problem | Managers may not maximize profits (ownership ≠ control) |

Key Conditions

Long-Run Competitive Equilibrium:

P = MC = min AC

π = 0

Entry condition: π > 0 → firms enter

Exit condition: π < 0 → firms exit